Scientific update

Innovation and risk-averse firms: Options on carbon allowances as a hedging tool

This research took place as part of the NORAD-funded project "Options Market and Risk-Reduction Tools for REDD+," which aims to help design, catalyze and launch pilot options transactions for REDD+ credits, attracting private companies and investors to finance high quality results-based REDD+ programs over near and medium terms.

The project aims to design complementary instruments to reduce risks for both buyers and sellers of jurisdiction-scale REDD+ credits, and make the most effective use of limited public funds to leverage private financing and supply development.

The Methods for Economic Decision Making under Uncertainty (MEDU) group applied a real options approach modeling stochastic carbon-saving technology costs and stochastic CO2 costs. Assuming that firms are risk-averse, it was found that they value both the flexibility and risk reductions resulting from diversification across different (carbon mitigation) options.

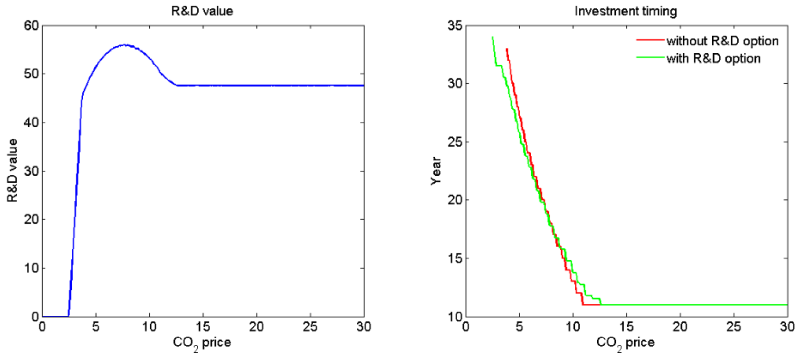

Figure 1. R&D value and investment timing as a function of the CO2 starting price (EUR/ton).

Figure.

References

[1] Szolgayová J, Golub A, Fuss S (submitted). Innovation & risk-averse firms: options on carbon allowances as a hedging too. Energy Policy.

Collaborators

Mercator Research Institute on Global Commons and Climate Change (MCC), Berlin, Germany;

EDF, USA.

Research program